Here are my top five takeaways from this year’s NCSHA Conference

1. Expand Access through Innovative Solutions (Not Just Tech)

Programs like Connecticut Housing Finance Agency’s (CHFA) SMART RATE program are leading the way in innovation. Smart Rate links student debt relief and rate buydowns to help first-time and first-generation buyers purchase homes sooner. Through Smart Rate, qualifying borrowers can receive a 1.125% reduction on their CHFA first mortgage interest rate, helping to offset student debt monthly payments and make homeownership more attainable. It’s a strong reminder that innovation isn’t just about tech, it’s about rethinking barriers that hold people back.

2. Compound Affordability and Environmental Sustainability

MassHousing’s Energy Saver Home Loan Program is proving that decarbonization and affordability can go hand in hand. By blending climate and home improvement goals, agencies are helping families save on energy while contributing to long-term environmental sustainability by reducing energy usage by at least 20%.

3. Reach Underserved Communities with Cultural and Community Responsiveness

Oregon Housing and Community Services’ (OHCS) Culturally Responsive Down Payment Assistance program is meeting communities where they are, and channeling resources through trusted local and Tribal organizations. OHCS awards funding to nonprofit organizations that have the capacity, skills, and infrastructure to support homebuyers in a culturally responsive way or reach communities in rural areas that are traditionally underserved by homeownership organizations. Down Payment Assistance-Culturally Responsive and Rural Organizations (DPA-CRRO) program-funded organizations disbursed almost $6.7 million to 209 homebuyers, with an average of $32,020 per homebuyer for homes across Oregon that cost, on average, $335,071.

4. Impact Data Drives Action

State housing agencies in Minnesota and Kentucky are using clear, accessible data to reframe housing as economic infrastructure. When we connect data to positive community outcomes, housing policy becomes more urgent and actionable.

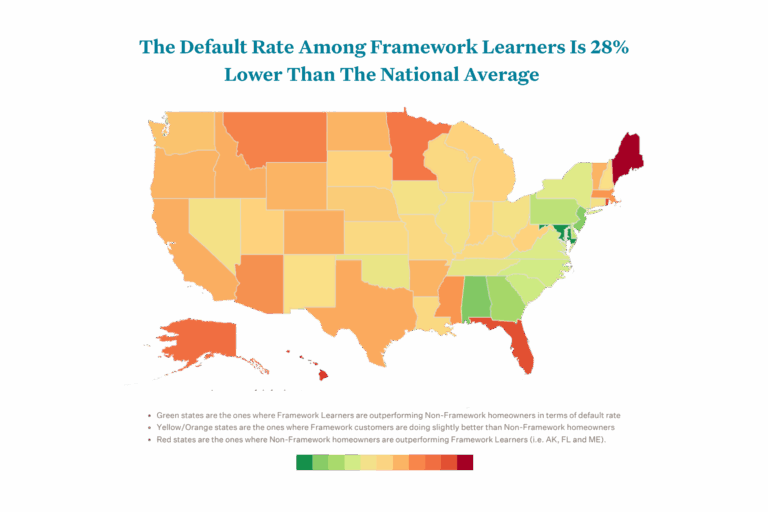

At Framework, we’ve seen that firsthand through our 2nd Annual Homeownership Confidence Report, where we gathered data from hundreds of homeowners to highlight their real experiences after closing. One standout insight is that Framework learners have a default rate that’s 28% lower than the national average, showing that informed buyers are more confident and more likely to sustain their homes. These numbers highlight the stories of the humans behind them, so housing professionals see where homeowners may need additional support and where to step in to make a long-term impact.